Media Summary: Computational Finance Lecture 10- Monte Carlo A brief overview of why I was rejected from Two Sigma. The DeepONets for Finance: An Approach to Calibrate the

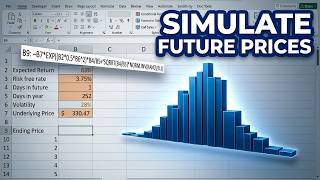

Using Heston Model To Simulate Stock Prices - Detailed Analysis & Overview

Computational Finance Lecture 10- Monte Carlo A brief overview of why I was rejected from Two Sigma. The DeepONets for Finance: An Approach to Calibrate the Full workshop available at www.quantshub.com Presenter: Roger Lord: Head of Quantitative Analytics, Cardano Within this ... MattMacarty **Predict Market Volatility: Monte Carlo