Media Summary: Master Quantitative Skills with Quant Guild: Join the Quant Guild Discord server here: ... In this video, we show how we can use put-call parity to build on our previous work and get the In this detailed video, we present "Decoding the Black-Scholes

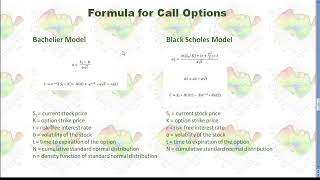

Python Bachelier Model Simulation In 3 Minutes - Detailed Analysis & Overview

Master Quantitative Skills with Quant Guild: Join the Quant Guild Discord server here: ... In this video, we show how we can use put-call parity to build on our previous work and get the In this detailed video, we present "Decoding the Black-Scholes Welcome to Financial Mathematics. In the 8th lesson we consider different topics. In this first video we look at the value of a EU ... Procedure for simulating the Ornstein-Uhlenbeck process in Case 1: Fixed Prepayment Rate Case 2: Input attributes, coefficients and values of the attributes Case

HE WAS THE FIRST TO USE ADVANCED MATHEMATICS TO STUDY FINANCE For courses on Credit risk