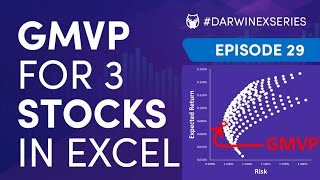

Media Summary: MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... ... correlation between those returns is negative 20% so I'm going to try to find the describe and interpret the minimum-variance and efficient frontiers of risky assets and the global

Minimum Variance Portfolio Table - Detailed Analysis & Overview

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... ... correlation between those returns is negative 20% so I'm going to try to find the describe and interpret the minimum-variance and efficient frontiers of risky assets and the global 4.14. Global Minimum Variance GMV Portfolio This simple example helps clarify how to solve for weights when constructing a This is an excerpt from our comprehensive animation library for CFA Level I candidates. For more materials to help you ace the ...

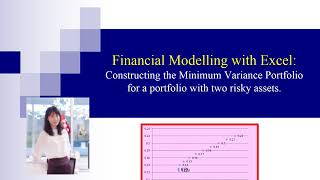

Financial Modelling with Excel. Measuring expected return and risk. Investment opportunity set.