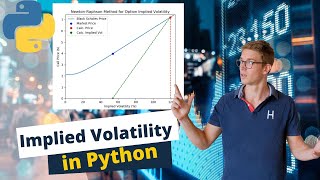

Media Summary: In this video we have discussed about a powerful financial library, and tried to Unlock the power of the Black-Scholes model A quick, impromptu video answering a viewer's question on if one can

Calculating Option Price And Iv Using Mibian In Python - Detailed Analysis & Overview

In this video we have discussed about a powerful financial library, and tried to Unlock the power of the Black-Scholes model A quick, impromptu video answering a viewer's question on if one can Yes, on this channel we've used the Black-Scholes For Intuitive Explanation for Implied ... Tutorial on creating a Black Scholes Merton Model within